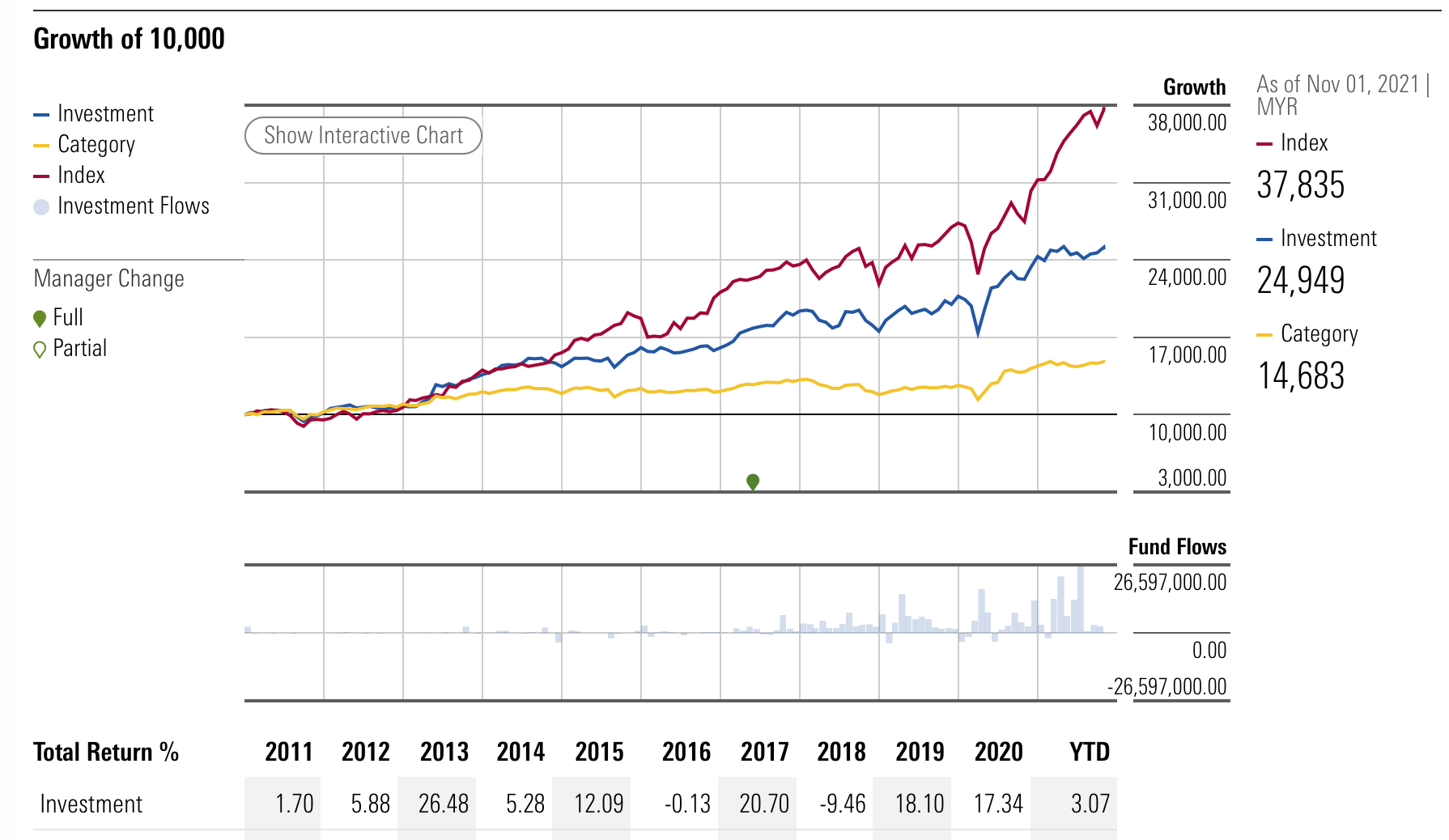

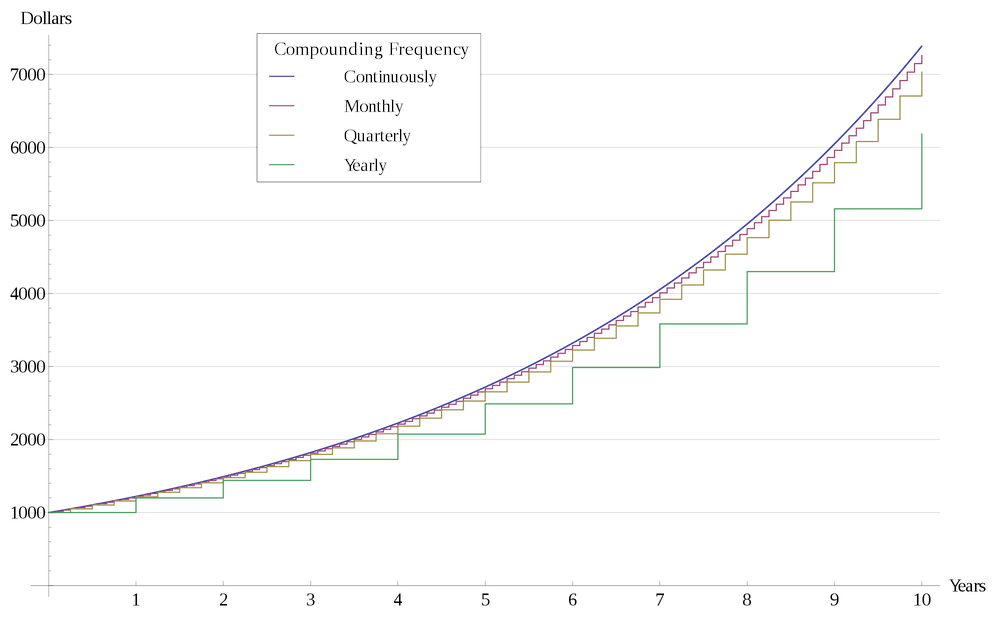

Berapa yang kita dapat simpan hari ini menentukan masa depan persaraan November 12, 2021November 12, 2021